Select Language:

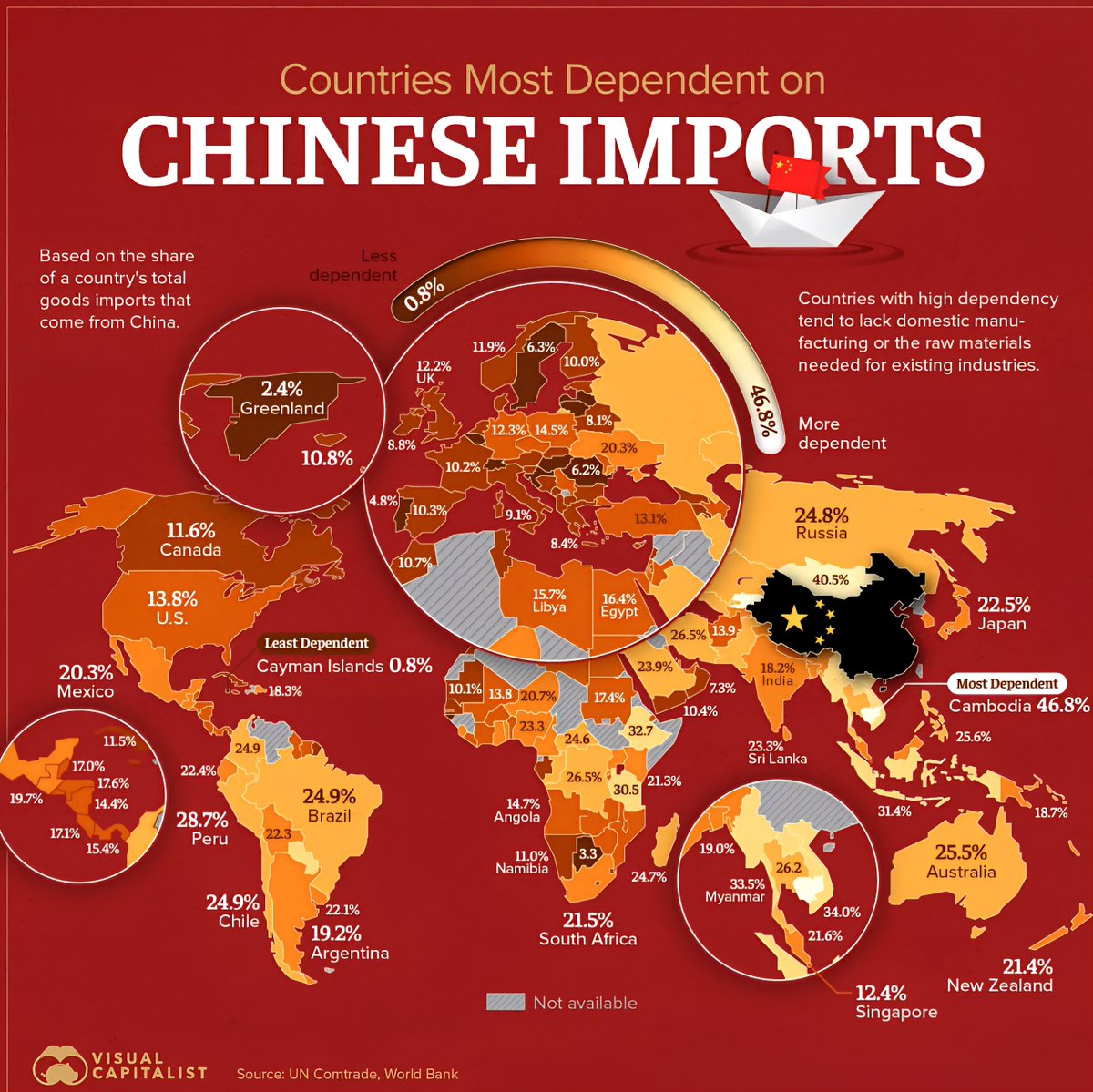

Cambodia Leads the Way with Nearly Half of Its Imports Originating From China

Cambodia remains the most heavily reliant on Chinese imports globally, with 46.8% of its total imports coming from China as of 2025. This dependence underscores the country’s integration into the Chinese supply chain, particularly in textiles, electronics, and infrastructure materials. The reliance also raises concerns about economic vulnerability should trade relations shift or disruptions occur. Despite efforts to diversify, Cambodia’s dependency remains a critical aspect of its trade strategy.

Kyrgyzstan and Hong Kong Close Behind — Broad Regional Dependence

Kyrgyzstan comes second, with 45.8% of its imports originating from China, highlighting Central Asia’s reliance on Chinese goods. Hong Kong follows closely, with 40.9%, emphasizing China’s dominance as a trade hub in the region. These figures reflect broader regional integration, with Chinese manufacturing and technology sectors serving as essential links for these economies.

Southeast Asia’s Growing Dependency on Chinese Goods

Vietnam and Myanmar occupy significant positions, importing 34.0% and 33.5% of their goods from China, respectively. These nations have expanded manufacturing sectors that are tightly linked with Chinese supply chains, especially in electronics and garments. As regional economies continue their growth trajectories, their dependence on Chinese imports is expected to deepen unless diversification strategies are implemented.

Africa’s Increasing Ties to China

Ethiopia (32.7%) and Paraguay (32.5%) feature prominently among the top dependent countries outside Asia. Ethiopia, with its expanding textile industry and infrastructure projects under China’s Belt and Road Initiative, exemplifies this trend. Paraguay’s reliance on Chinese machinery and electronics mirrors a broader shift toward China as a primary trading partner across the continent.

Asian Neighbors and Major Economies

Indonesia (31.4%) and Tanzania (30.5%) illustrate that even emerging economies are highly intertwined with Chinese trade networks. Meanwhile, regional financial hubs like Macao (30.1%) and Laos (29.8%) demonstrate the multifaceted nature of dependence, including services and manufacturing.

Notable Latin American and Middle Eastern Dependence

Peru (28.7%) and Pakistan (28.3%) show significant reliance, underscoring how Chinese imports influence sectors from industrial supplies to consumer electronics in these regions. In the Middle East, Saudi Arabia (23.9%) and Egypt (16.4%) also exhibit substantial dependence, often linked to energy imports and oil trade, emphasizing China’s strategic material needs.

Dependency Trends in Australia and Canada

Australia (25.5%) and Canada (11.6%) reflect a mixed dependency pattern, influenced by trade in minerals, technology, and goods. The divergence illustrates differing economic structures but highlights the global reach of Chinese manufacturing.

Dependence in European and African Nations

European countries show comparatively lower dependence, with Germany (12.3%) and the UK (12.2%) relying less on Chinese imports. Yet, some African nations—like Ghana (18.7%) and Nigeria (23.3%)—demonstrate notable reliance, often impacting local manufacturing and consumer markets.

The Broader Global Context

The dependency figures outline a complex web of international trade relationships, many of which are set to evolve as geopolitical and economic factors shift. Countries with high dependence risk exposure to Chinese trade policy changes, supply chain disruptions, or shifts in global manufacturing hubs.

Conclusion

As of 2025, China remains the central trading partner for many nations worldwide, especially in Asia, Africa, and parts of Latin America. While this dependence fuels economic growth and development for some regions, it also poses risks that could impact global stability if dependencies are not managed carefully. Countries are increasingly aware of the necessity to diversify their supply chains and decrease vulnerability to external shocks, but the extent of dependency suggests that China will continue to play a dominant role in global trade for the foreseeable future.

Source: UN Comtrade, World Bank via Voronoi by Visual Capitalist