Select Language:

The fate of Cursor hangs in the balance, caught between two rapid-moving forces: the maturity of AI autonomous coding and the company’s own transformative evolution. While Cursor continues to grow at an impressive pace, some industry observers are beginning to question its future viability, framing its rise and potential decline as two sides of the same coin.

As of February 2026, Cursor’s annual revenue surpassed $2 billion — a dramatic jump from just $1 billion three months prior. This explosive growth makes it the fastest company in Silicon Valley to reach such a milestone from zero, with over 150 million lines of enterprise code being generated daily through its platform. More than two-thirds of Fortune 500 firms are using Cursor, and new funding rounds are underway, with the company’s valuation aiming towards $50 billion. A16z partner Martin Casado publicly declared, “Excluding invested capital, Cursor is the fastest-growing company I’ve ever seen.”

However, that same month, a small startup called Valon announced that over 90% of its team had switched from Cursor to Anthropic’s Claude Code. Valon’s CEO, Andrew Wang, stated that for the same tasks, Claude Code completed work ten times faster. While a decision by a single small company might seem insignificant in the face of Cursor’s massive scale, it sparked a heated debate on social media about whether Cursor’s era might be nearing its end. Rumors of Cursor’s demise began trending among developer communities, prompting Casado to respond widely, emphasizing that the data shows no signs of decline and that Cursor continues to succeed on measurable metrics.

Yet, amid the confident narrative, a tougher question emerges: when a company’s performance metrics look stellar, but a critical segment of industry players expresses widespread unease, should signals be trusted more than signals?

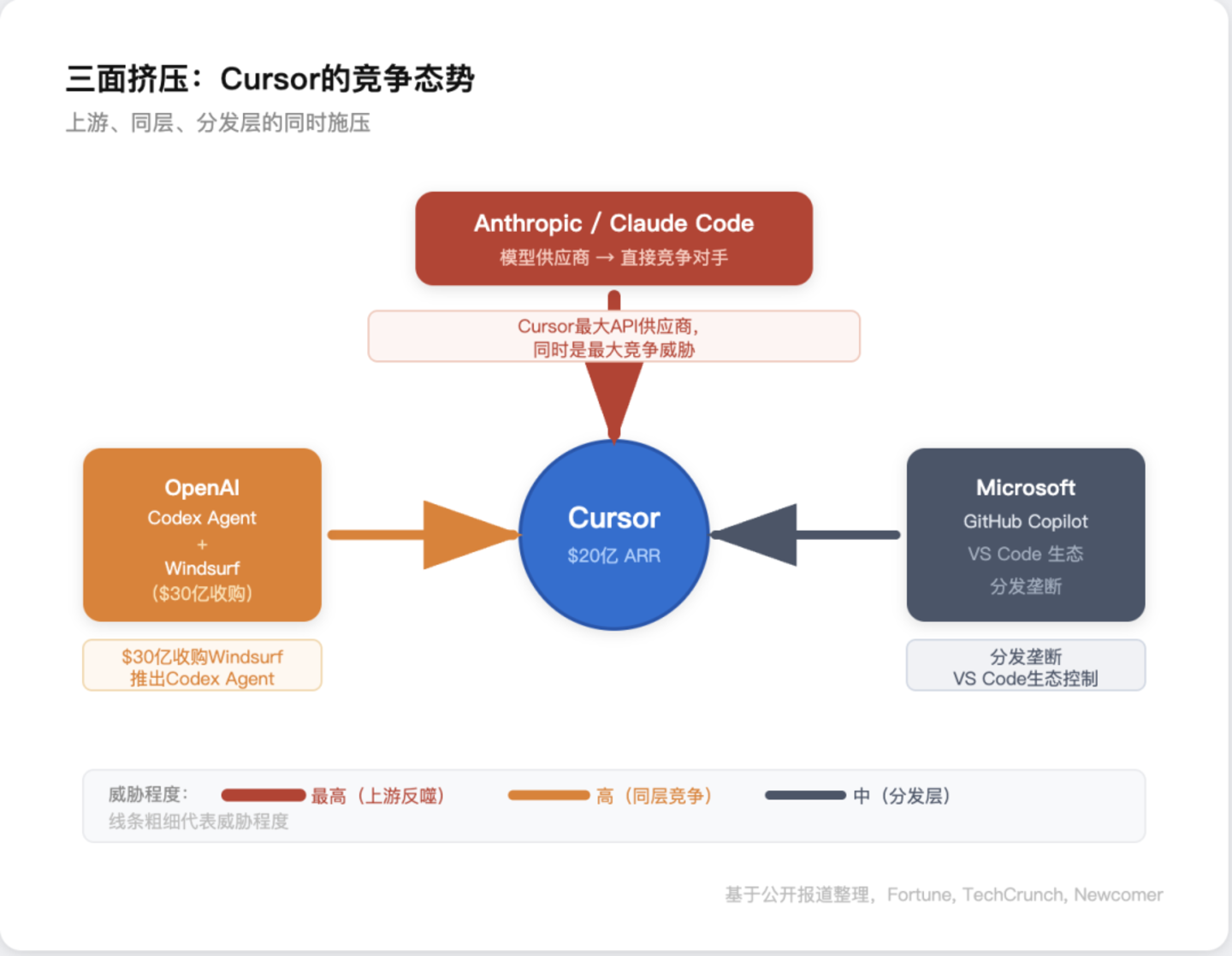

Looking deeper at the data that’s not immediately visible, the situation becomes more nuanced. Claude Code was released in May 2025 and, by early 2026, had achieved an annualized revenue of over $2.5 billion — surpassing Cursor’s figures in absolute value. Anthropic remains a major model provider for Cursor, with its models powering much of Cursor’s functionality, and Anysphere, a significant customer of Anthropic, underpins this dependency. Meanwhile, OpenAI bought Windsurf, a direct competitor to Cursor, for $3 billion. Reports also indicate that OpenAI tried to acquire Cursor itself but was unable to reach an agreement. Subsequently, OpenAI launched Codex Agent, a cloud-based autonomous coding AI that saw over 1 million downloads in its first week, extending the competitive pressures through dominance in cloud AI services, especially with Microsoft’s GitHub Copilot.

Yet, the most impactful challenge to Cursor’s dominance isn’t a direct competitor — it’s the broader shift in software development paradigms. Zach Lloyd, CEO of Warp, encapsulated this by saying, “I don’t believe in ‘Cursor is dead,’ but I do believe that ‘IDEs are dead.’ Software isn’t made like that anymore.” His insight pivots the debate from product comparisons to envisioning the future of coding. If software development evolves to where natural language commands by developers are understood and executed autonomously by AI, then traditional IDEs — no matter their intelligence — could become obsolete.

Casado’s confidence in the data contrasts with developers’ growing frustrations. This discrepancy underlines a vital understanding: a company’s situation is layered, with multiple dynamics operating simultaneously at different speeds. The public narrative and valuation tend to shift rapidly, driven by media and market sentiment, changing daily or weekly. Product performance and revenue figures fluctuate monthly or quarterly, while deep shifts in technological paradigms and industry structure evolve over years.

In this case, while Cursor’s revenue and enterprise contracts have maintained strong growth, signaling success to the outsider, developer sentiment reflects a more profound unease—an indicator that the underlying technological paradigm is shifting from assisted to autonomous AI coding. Recent reports from SemiAnalysis estimated that by February 2026, Claude Code completed around 4% of all commits on GitHub — a small figure at first glance, but significant considering the rapid growth rate. Moreover, a survey by Pragmatic Engineer revealed that nearly half of developers considered Claude Code their favorite AI coding tool, with Cursor occupying second place.

This growth suggests a fundamental transformation is underway, even if it hasn’t yet fully reflected in Cursor’s financial reports. Currently, a large portion of Cursor’s revenue — around 60% — comes from enterprise clients, who are slower to migrate to newer tools. Meanwhile, individual developers and startups are quietly switching to Claude Code, but this loss is temporarily masked by the expansion of enterprise contracts. Over time, however, the shift in developer preferences will exert pressure on company contracts, as developers are often the ultimate influence on organizational procurement.

The difference in pace between developer behavior and strategic enterprise decisions indicates an impending challenge for Cursor. Developer migration acts as a bellwether; if early adopters abandon Cursor en masse, companies will follow. Casado recognizes that while the low-level infrastructure and core user base remain stable, the increasing confidence and excitement at the developer level signal an impending reset.

So, why are developers leaving now? The answer lies less in individual product shortcomings and more in the evolution of the entire AI coding ecosystem. Cursor’s rise was driven not by a linear improvement but by aligning multiple fast-moving industry layers: market narrative, valuation, product, and industry paradigm. During 2023-2025, at least two slow-moving layers shifted in Sync—large language models’ coding efficiency crossed a threshold from novelty to necessity, and software development workflows began to be redefined by AI.

This convergence boosted Cursor into a lofty flight, but the momentum cannot be assumed to continue forever. As the airflow that propelled it abates or shifts direction, the fundamental question becomes whether Cursor can solidify its position within a deeper technological infrastructure. Companies like NVIDIA have embedded their architectures, such as CUDA, into the foundational AI ecosystem—an enduring position unlikely to be lost even as market narratives cool.

What about Cursor? While it benefits from the current positive sentiment, much of its success remains superficial. Its core features — autocomplete, file refactoring, inline editing — are highly valued but are merely surface-level functionalities. It is still heavily reliant on external models, primarily Anthropic, and the revenue generated from API calls to these models constitutes a significant and ongoing expense. As expenses grow, the profit margin diminishes, especially given that each user interaction consumes costly inference resources.

Thus, despite impressive growth, Cursor faces a stark reality: it is flying high on the inertia of the initial wave of AI adoption, but the underpinning of its flight—dependence on third-party models—remains fragile. Internal efforts to develop its own models, like the recent release of Composer 2, a large language model based on open-source Chinese models, highlight both ambition and vulnerability. While internally training models offers a potential shift toward independence and higher margins, it also demands resources and expertise far beyond the company’s current capacity.

In conclusion, Cursor’s recent trajectory underscores its strategic predicament: it is caught between an industry shifting rapidly towards autonomous AI coding and the slow, painstaking process needed to embed deeper infrastructure and genuine independence. If the momentum of the broader AI paradigm shift accelerates faster than Cursor’s evolution, it risks a hard landing despite its headline-grabbing valuation. Conversely, if it can navigate this transition successfully, it could redefine itself from a mere application layer to a powerful platform with its own models.

Ultimately, the question isn’t just about product excellence, but about whether Cursor can maintain its place in a reconfigured software world—one where control over core AI capabilities might determine who rules the future of software development. And in that race, the clock is ticking.